This page is optimised for desktop viewing

·

This page is optimised for desktop viewing ·

Delivering an end-to-end digital lending experience

Role - Senior UX Designer @ Backbase

Platform - Web and App

Scope - An end-to-end loan origination experience

Team - PM, BA, User Research, Engineering-manager, Front-end, Back-end, QA

*View this image in more detail by clicking on it.

Summary

Backbase’s business-orchestration product, ‘FLOW’ has a strong foothold in the digital-onboarding space and wanted to capitalise on this momentum by entering the lending-origination space.

Recruited as a founding designer for a newly created ‘Digital Lending’ value-stream, I was tasked with getting a product-offering to market and then maturing the product into a credible, end-to-end product suite that translated complex orchestration logic into seamless user experiences that banks wanted to adopt as part of their digital-transformation project.

Opportunity

While the initial objective was to validate 'FLOW' as a viable lending-origination product accelerator, there was also a strategic opening for the design-function to pivot being delivery-focused to a core product partner. I used this momentum to influence the long-term roadmap, demonstrating that the design function is not merely an 'engineering unblocking mechanism' but a critical driver of product strategy and stakeholder alignment.

My role

The following outlines my three-year tenure within the Digital Lending value-stream, where I operated as a lead design voice across the entire service lifecycle and framed design as a key product stakeholder.

End-to-end design delivery: I bridged the gap between vision and execution, communicating high-level concepts to technical leads to uncover 'unlocks' before refining them into detailed, production-ready assets.

Business intelligence: Collaborating closely a business analysts, I organised opportunities to engage with senior bank stakeholders to understand how their complex business requirements could be translated into intuitive lending experiences and product opportunities.

Strategic discovery: I co-created and facilitated robust research plans to maintain a constant thread of user insights that directly informed our experience maps, product definitions and strategic opportunities.

Systems thinking & scalability: I championed scalability by managing lending specific components, ensuring that unique patterns were either standardised within our design system or logically integrated into the product’s codebase.

By combining these skills, I moved beyond 'delivering screens' to delivering validated design rationale, providing stakeholders with the confidence to make informed product decisions.

Milestone #1

Getting a product to market

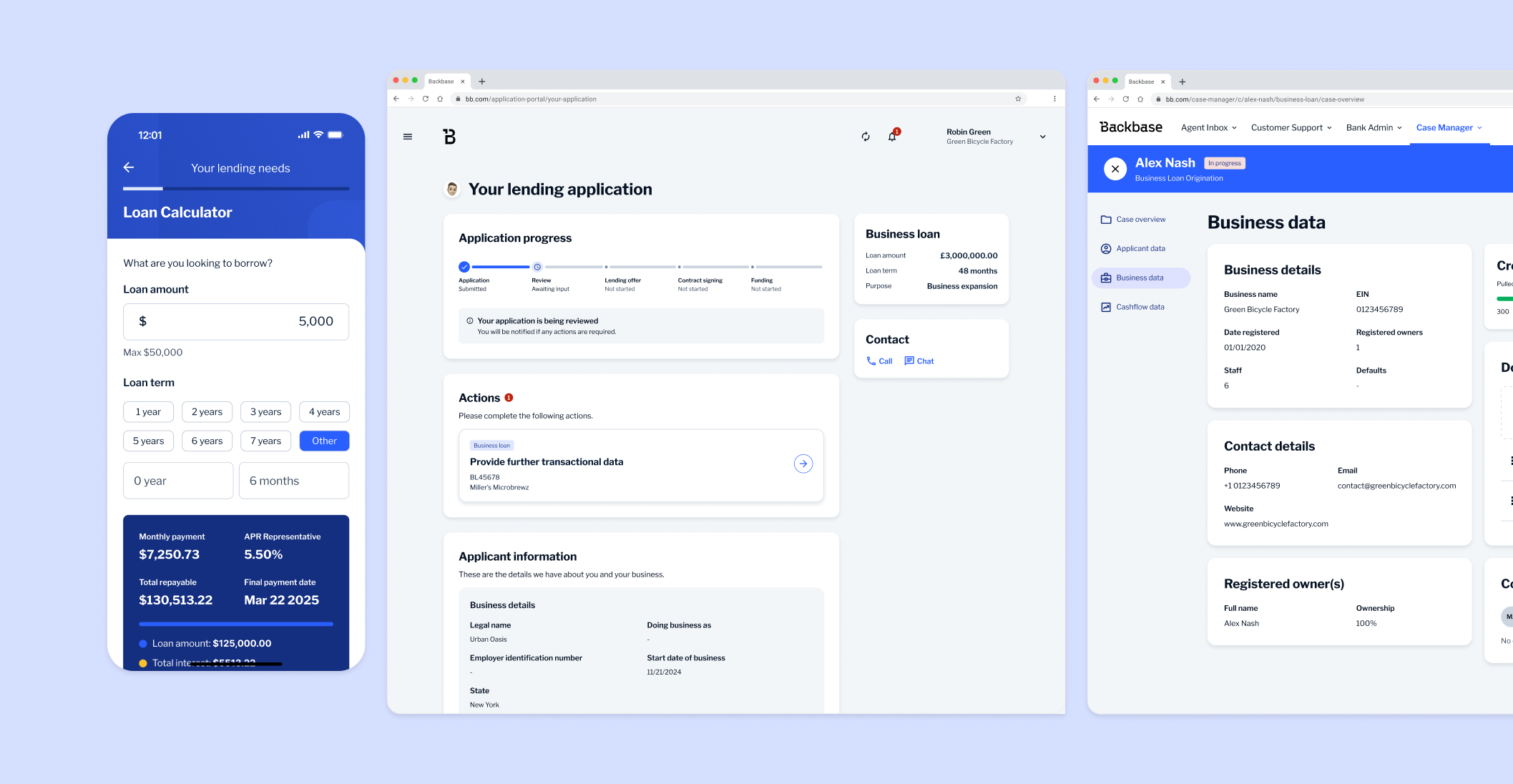

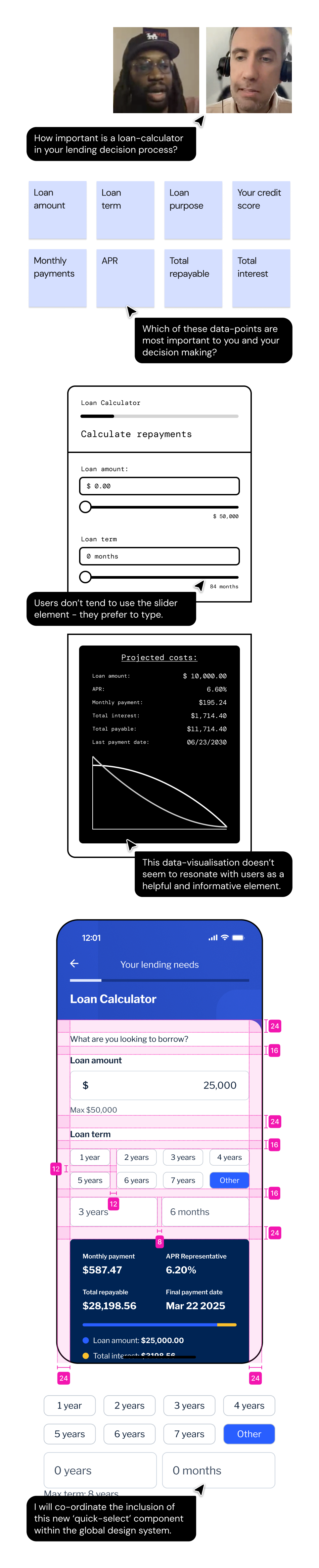

The immediate objective was clear: bridge critical experience gaps with the loan calculator and pre-qualification journeys to unlock a viable, end-to-end product - up to pre-qualification decisioning - for market launch.

From a process perspective, I faced a dual challenge: I needed to maintain high-velocity design delivery to sustain engineering momentum, while simultaneously establishing a formal framework that would encourage cross-functional partnership with product and technical stakeholders on future initiatives.

Demonstrating value

In a two-sprint timeframe, I delivered the following milestones…

Discovery interviews: These were used to determine the specific value existing loan calculator designs provided within the user's lending journey. These insights defined the core themes for the subsequent design explorations.

Card-sorting exercises: This allowed me to identify the critical data-points users required to make their informed borrowing decisions. These insights helped influence the information-architecture with the designs.

Iterative concept testing: I tested a variety of low-level prototypes to optimise and understand the typical interaction models users required for adjusting loan amounts and durations. As effective patterns began to narrow, I increased prototype fidelity to validate the experience within a high-fidelity, contextual environment. These insights helped steer and direct the design approach.

Design system contribution: In identifying a requirement for a ‘quick-select’ component for loan terms, I collaborated with the Global Design System squad to develop and integrate this new pattern within the product and ensuring scalability was at the core of its approach.

The velocity at which I validated these decisions served as a powerful demonstration of the value design could bring to the product development process. It helped establish a foundational partnership with the engineering team that resulted in less hard-coded product and a greater need for design-led specification as a source-of-truth.

Outcomes

Following an additional four-week development cycle, a functional MVP (Minimum Viable Product) was delivered. This not only empowered the sales team to engage existing and prospective clients with a tangible offering but also provided a stable environment for rigorous evaluative testing.

While the engineering team worked towards this deliverable, I collaborated with the User Researcher to architect a robust testing framework that would ensure we could capture live user data to inform the next phase of the product roadmap.

Milestone #2

Establishing feedback loops

With a tangible product at my disposal, I established a comprehensive research framework designed to balance long-term product strategy with immediate tactical validation. This dual-track approach ensured that our roadmap was driven by both commercial requirements and user evidence.

Customer validation: By maintaining a close feedback loop with the sales team, I gained direct access to the key decision-makers within partner banks. I regularly joined these sessions to observe how our value proposition resonated at a high level, ensuring the end-to-end experience aligned with institutional expectations and procurement needs.

Iterative usability testing: I implemented a weekly testing cadence via UserTesting.com to monitor the product's performance with end-users. These sessions were critical for identifying friction points and service failures, allowing for rapid iteration. Beyond immediate fixes, these insights also informed the design of the post-qualification journey—helping to extend the experience from the initial decision through to successful fund disbursement.

Influencing a new approach

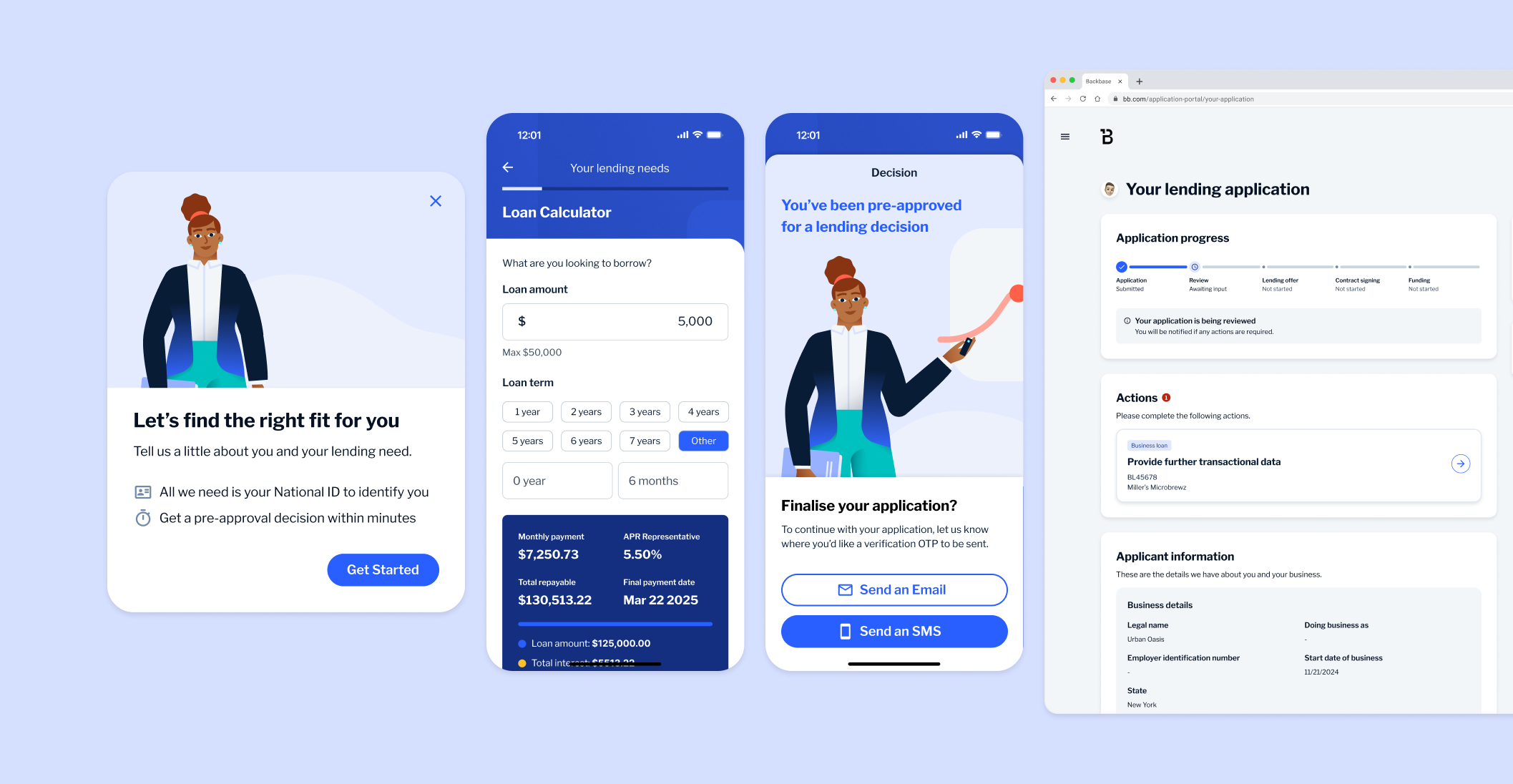

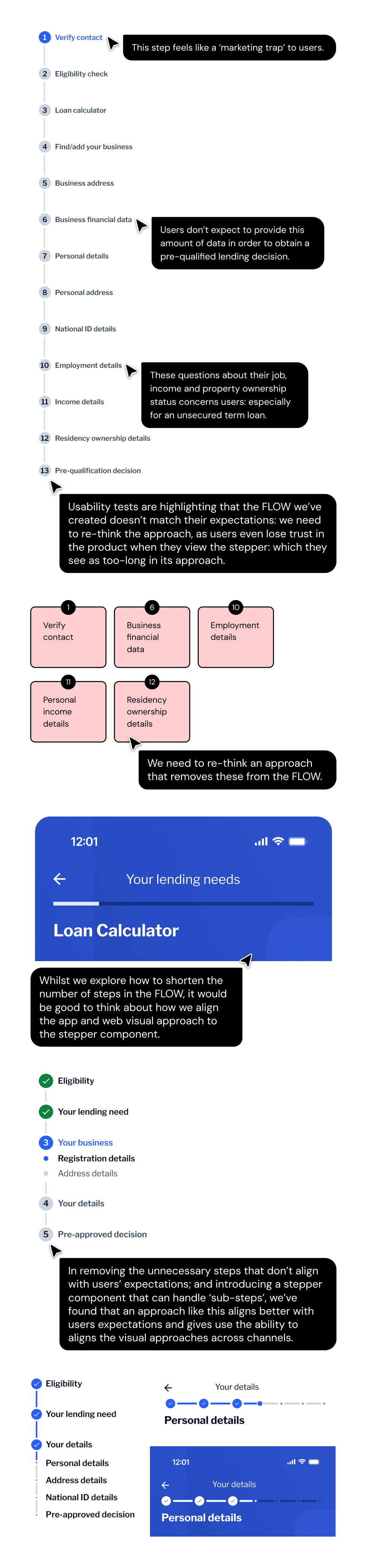

Through dual-track testing with end-users and banking clients, a significant friction point emerged: the length of the application form directly contradicted the 'quick and easy' value proposition. Users perceived the journey as cumbersome, creating a misalignment between the brand promise and the actual experience.

To resolve this, I took the following strategic actions:

Challenged product approach: While the initial goal was to demonstrate how quickly a new lending journey could be assembled using legacy components, I argued that we had moved past the "proof-of-concept" phase. Using my research as evidence, I advocated for an 'opinionated' design approach—shifting from a generic assembly of parts to a bespoke, optimised lending experience that prioritised user conversion by delivering what end-users actually wanted.

Technical negotiation: To assess the impact of streamlining the journey, I collaborating heavily with product and engineering. By diving into the technical constraints, I identified that the necessary improvements could be achieved by amending FLOW’s API logic rather than rebuilding the platform architecture. This ensured we could deliver a high-impact fix without significant technical debt and with relative speed.

Prototyping: With the technical path cleared, I developed prototypes focusing on a redesigned stepper component. My objective was to improve upfront transparency regarding the application length, testing how clearer expectations influenced user intent and reduced mid-flow drop-off rates.

Outcomes

In pivoting the product strategy to align with user expectations yielded immediate commercial and experiential results. We observed a significant increase in positive feedback from the sales team, and more importantly, a rise in customer adoption of the 'opinionated' product model. By delivering a highly optimised default experience, we reduced the need for bespoke customisations on project, effectively shortening the time-to-market for partner banks.

From an end-user perspective, analytic analysis confirmed a measurable increase in completed pre-qualification journeys across live implementations. With this initial friction resolved, the next strategic objective I saw value in going after was optimisation of the conversion funnel between the pre-qualification decision and full application submission.

Milestone #3

Uncovering opportunities

Through extensive research sessions with both end-users and banking staff, I identified two systemic service failures that were undermining the lending experience:

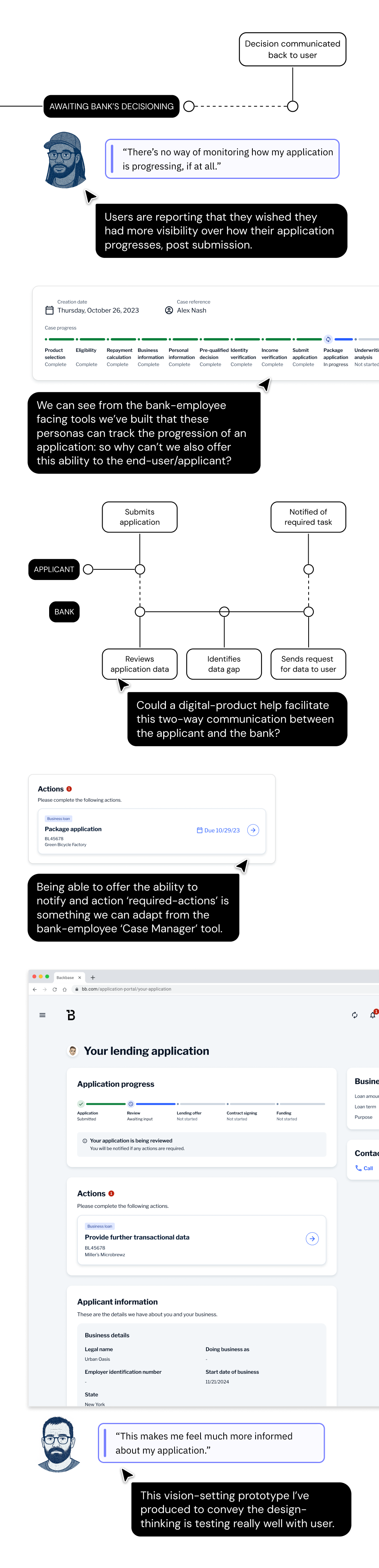

Lack of status transparency: Users frequently described feeling 'left in limbo' after submitting an application. This 'waiting game' was a direct result of a lack of status playback, which created significant anxiety and reduced trust in the digital service. If and when contact was made with the user, it came via email and secure-web-links.

Operational friction in underwriting: In-depth sessions with underwriters and application packagers revealed a high rejection rate due to incomplete applications. This mirrored a critical user pain point: many users had to re-submit applications from scratch, often incurring a second, unnecessary credit check due to the lack of guidance in the initial submission flow.

These insights presented a clear opportunity: to provide an experience that would reduce both user frustration and the administrative burden on the bank.

Design thinking

I set out to determine if a digital product could resolve these communication gaps and significantly reduce premature application rejections.

To validate this hypothesis, I led the following initiatives:

Multidisciplinary workshops: Using the research insights as a catalyst for discussion, I facilitated a series of workshops with product and engineering leads. We deep-dived into the systemic causes of rejection and ideated how the platform could evolve to resolve these friction points.

Prototyping a vision: There were two critical experiences that this application-communication tool required: real-time application tracking and a streamlined document upload journey. With both of these journeys already existing within the ‘Case Manager’ product (originally design for internal bank staff), I adapted them into this bespoke, user-facing experience.

Validation: With internal stakeholder buy-in secured, I translated the prototype into a rigorous discovery research plan. After achieving user validation, I partnered with the sales team to present the solution to prospective customers, ensuring the concept was fully compliant with banking process standards and commercial expectations.

Traction obtained

As the prototype gained significant traction during client demonstrations, our sales team identified a strong strategic appetite for its inclusion in the product roadmap. However, before approaching senior leadership for development investment, we needed to validate the concept at scale during Backbase’s flagship ‘Engage’ conference—a global forum where international banking leaders assess new product innovations against their digital roadmaps and technical stacks.

To ensure the concept resonated on this global stage, I collaborated with the Global Brand team to architect a narrative and script that seamlessly integrated with the prototype’s functionality. I also acted as a lead advisor to the sales team, refining the pitch and overseeing the prototype’s performance to ensure a high-impact presentation.

Outcomes

The product vision was received extremely well and successfully secured the required corporate investment for full-scale development. To support this expansion, new squads were required, which necessitated an increase in design capacity.

I participated heavily in the recruitment process for an additional designer, ensuring we brought in the right talent to sustain our momentum. Following a successful hire, I took ownership of their onboarding and mentorship—imparting my domain expertise in digital lending and establishing a collaborative framework to ensure design consistency across the expanding value stream.

Milestone #4

The bank employee experience

With the customer-facing journey clearly defined, I pivoted to the internal product offering, focusing on empowering bank employees with the tools necessary to manage and process these new lending streams.

Data handling

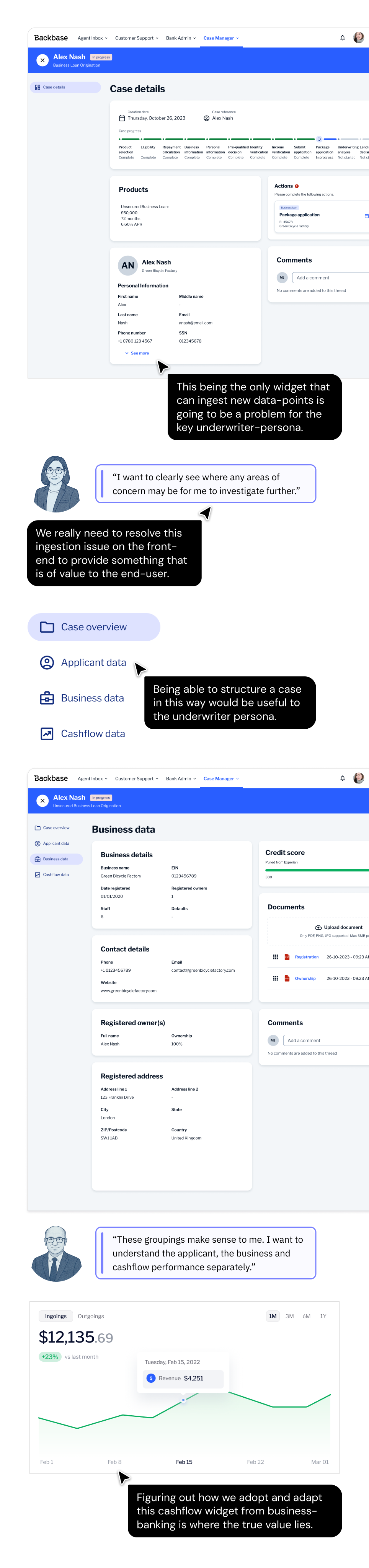

Unlike simple account onboarding, lending applications demanded a significantly higher volume of data points to facilitate complex risk analysis. When attempting to integrate this influx of data into the existing ‘Case Manager’ framework—which was originally optimised for onboarding—I identified a critical architectural flaw.

Lack of flexibility within the UI: The product was designed to aggregate all data into a single widget on one page. However, my research with underwriters revealed a requirement for distinct data separation. To conduct efficient risk analysis, they needed information categorised into specific domains: applicant-data, business-data, product-data, and financial performance/cashflow-data.

The 'one-page' constraint was failing this persona’s primary need: the ability to quickly isolate and scrutinise specific risk factors without navigating a wall of undifferentiated data.

Solving this issue

While the engineering team addressing the technical infrastructure for supporting additional UI components, I focused on the structural logic and data density challenges.

Information architecture: Operating on the premise of a more flexible UI, I conducted card-sorting exercises with underwriters to establish a logical hierarchy for the applicant data. This ensured that the new multi-page structure aligned with their mental models and decision-making workflows.

Cashflow analysis: Assessing a business's financial health is the cornerstone of risk analysis—often exceeding the complexity of standard KYC (Know Your Customer) or credit checks. To manage the high density of data found in multi-month financial reports, I avoided 'reinventing the wheel' by identifying that the existing 'Cashflow Forecasting' modules within the Business Banking domain as a key solution for the underwriter persona within the Case Manager. I worked across teams to repurpose these components within this context, ensuring underwriters had the sophisticated tools needed for their financial scrutiny without the team incurring unnecessary development overhead.

Outcomes

By ensuring all identified use cases were technically addressed via this UI re-structuring, we provided banking clients with a significantly more flexible and scalable Case Manager. This architectural shift not only increased the product’s market value but also represented a critical milestone for our team: the realisation of a comprehensive, end-to-end product experience. For the first time, we could demonstrate a seamless journey to stakeholders and customers—from initial applicant submission through to final underwriter approval and fund disbursement.

Key reflections

From a product perspective, there were many positives to take-away…

Product sales were successful and helped the value-stream meet and exceed its ARR targets.

While the value stream’s initial mandate focused on developing an Unsecured Business Loan (USBL) offering, the launch of the 'Application Centre' initiated a pivot toward a broader retail-lending origination product-line being spun-up.

The Application Centre was positioned as a modular, standalone asset; it empowered banks to generate high-conversion entry points for existing customers, independent of the core USBL product line.

From a personal perspective…

I became a knowledge expert the lending-domain.

I effectively demonstrated how valuable design and its insight-driven focus could be to the product engineering process.

I operated as a cross-functional lead, collaborating with many parts of the business to ensure the lending journey was seamlessly integrated into the existing business and retail banking ecosystems.

With my active role in scaling the design function; this experience in recruitment, mentorship, and team-shaping has solidified my ability to lead multidisciplinary squads and drive high-impact design strategy.